How Much Does Credit Score Decrease After a Car Loan? 2026 Top Tips

If you’re considering taking out a car loan, you’re probably wondering to yourself, “how fast will a car loan raise my credit score” or how much does a car loan decrease your credit score? The short answer is: it can affect your score, but the extent of the impact depends on several factors, including your current credit profile and how you manage the loan.

While a car loan may cause a temporary dip in your credit score, it can also be a powerful tool for improving your credit in the long run if managed properly.

In this blog post, we’ll explore the timeline for how long your credit score will be affected after taking out a car loan, the factors at play, and how you can use a car loan to boost your credit.

What Happens to Your Credit Score When You Take Out a Car Loan?

When you take out a car loan, there are a few key ways it will affect your credit score. Lenders look at your credit report to determine your creditworthiness, and a new loan affects several factors, including your credit utilization, payment history, and the type of credit accounts you have.

Here’s how a car loan can affect your credit score:

- Hard Inquiry: When you apply for a car loan, the lender will perform a hard inquiry (or “hard pull”) on your credit report. This can cause a temporary dip in your score by a few points. The effect of a hard inquiry is usually short-lived and typically only impacts your score for a few months.

- Credit Utilization: Your credit utilization ratio, which is the amount of credit you’re using compared to your total credit limit, makes up a significant portion of your score. A car loan doesn’t directly affect your credit utilization ratio, but if you use a credit card to make a down payment or to pay for other costs related to the car loan, your credit utilization may increase, which could lower your score.

- Credit Mix: Lenders like to see a healthy mix of credit accounts. When you add a car loan to your credit report, it improves your credit mix, as it adds installment credit to your profile. This can help your credit score in the long run, especially if you’re relying heavily on credit cards.

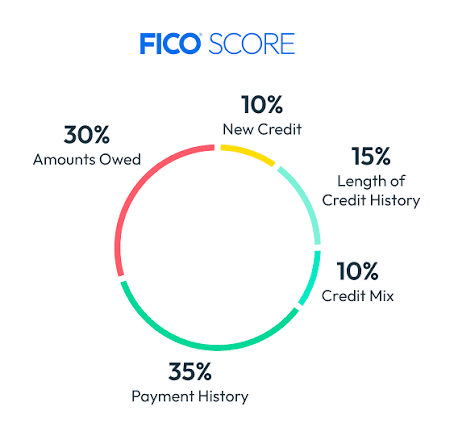

- Payment History: Your payment history makes up 35% of your credit score. As long as you make timely payments on your car loan, your score will likely improve over time. Missing payments, on the other hand, can have a significant negative impact on your credit score.

How Long Does It Take for a Car Loan to Affect Your Credit Score?

If you’re wondering how long it takes for a car loan to impact your credit score, here’s a breakdown of the short-term and long-term effects:

- Short-Term Impact (0-3 Months):

Initially, taking out a car loan may cause a small dip in your credit score due to the hard inquiry. This is typically a minor decrease, usually in the range of 5 to 10 points. During the first 30 to 60 days, you may not see significant improvement in your score, as credit bureaus will take some time to report the new loan and reflect your payment history. - Mid-Term Impact (3-6 Months):

After 3 to 6 months of consistent, on-time payments, you should start to see gradual improvements in your score. The credit bureaus will begin to notice your responsible behavior, and your credit score will likely begin to rise. This is when the positive effects of your car loan (such as improved credit utilization and payment history) start to take hold. - Long-Term Impact (6-12 Months):

The full benefits of a car loan on your credit score will likely become evident after 6 to 12 months of timely payments. Your credit mix will improve, and your payment history will have a positive impact on your score. If you’ve kept your credit utilization low and made on-time payments, your credit score should show a substantial increase.

Read Also: How Long Do Late Payments Stay on Your Credit Report? 2026 Update

Factors That Affect How Fast Your Car Loan Will Raise Your Credit Score

Several factors determine how quickly a car loan will raise your credit score. Let’s take a look at the most important ones:

- Payment History (35% of Your Score):

On-time payments are the most important factor in determining your credit score. By paying your car loan on time, you can gradually improve your score over time. - Credit Utilization (30% of Your Score):

A car loan can affect your credit utilization if you’re using other lines of credit to cover the car loan’s down payment or other associated costs. The lower your credit utilization, the better your score will be. - Credit Mix (10% of Your Score):

Adding a car loan to your credit report improves your credit mix, which can positively impact your score. This is especially important if you mainly rely on revolving credit accounts like credit cards. - Hard Inquiries (10% of Your Score):

A hard inquiry is made when you apply for credit, and it can temporarily lower your score by a few points. However, the effect of a hard inquiry is usually minimal and short-lived.

See Also: What is Revolving Utilization and How to Fix It From Hurting Your Credit

How to Maximize Your Car Loan’s Impact on Your Credit Score

If you want to make the most of your car loan and maximize its positive effect on your credit score, here are a few tips:

- Make Timely Payments:

Payment history is the most important factor in your credit score, so ensure that you make every car loan payment on time. - Keep Your Credit Card Balances Low:

Lower your credit utilization by keeping your credit card balances as low as possible. - Avoid Opening New Credit Accounts:

Too many new credit inquiries can hurt your credit score. Only apply for credit when necessary.

How Credit Veto Can Help You Improve Your Credit Score

If you’re looking to improve your credit score while making major financial decisions like buying a car, Credit Veto is here to help. We offer a range of tools to help you manage your credit score and maximize the impact of your car loan on your credit. Here’s how we can assist:

- Dispute Errors:

Credit Veto helps you identify and dispute errors on your credit report to ensure that your score is accurate. - Credit Monitoring:

Track your credit score and monitor changes in real-time, so you can stay on top of your progress. - Personalized Advice:

Receive actionable steps to improve your credit and make the most of your car loan’s positive effects on your score.

- Funding Opportunities

We connect you to lenders who approve real businesses, not just perfect credit scores. As your credit improves, so do your funding terms.

Final Thoughts

So, how much does a car loan decrease your credit score? The short answer is that the initial impact is minimal but temporary. By understanding how car loans affect your credit and taking proactive steps to manage your payments and credit utilization, you can maximize the benefits of your car loan and improve your credit score in the long run.

If you want to ensure your car loan is working for you, visit Credit Veto for expert guidance on how to improve your credit score and make informed financial decisions.

Ready to improve your credit score and manage your car loan effectively? Sign up for Credit Veto today to access our tools and resources that can help you fast-track your credit journey!

Frequently Asked Questions (FAQs)

How long does it take for a car loan to improve my credit score?

It typically takes 3 to 6 months of on-time payments to see improvements in your score.

Does a car loan hurt your credit score?

A car loan can cause a slight dip in your score initially, but it can improve your credit over time with consistent, on-time payments.

Can I get approved for a car loan with a 600 credit score?

Yes, it’s possible to get approved, but you may face higher interest rates and less favorable loan terms.

How Long Do Late Payments Stay on Your Credit Report? 2026 Update

How Long Do Late Payments Stay on Your Credit Report? 2026 Update  How Many Credit Cards Should I Have? Avoid These 4 Mistakes

How Many Credit Cards Should I Have? Avoid These 4 Mistakes  How to Check Personal Credit Report: 7 Easy Steps

How to Check Personal Credit Report: 7 Easy Steps  How a Credit Repair Course Can Improve Your Credit Score and Business Faster

How a Credit Repair Course Can Improve Your Credit Score and Business Faster  How Fast Will a Car Loan Raise My Credit Score? 2026 Real Timeline

How Fast Will a Car Loan Raise My Credit Score? 2026 Real Timeline  Vantage Score vs FICO: 7 Critical Truths Credit Pros Miss

Vantage Score vs FICO: 7 Critical Truths Credit Pros Miss