Everything You Need to Know About Your Credit Score and How It Affects You

From discovering what a credit score really is to understanding how they are calculated and understanding the different credit scores and factors that influence them, this guide contains everything you need to know about your credit scores.

Your credit score is one of the most critical financial metrics that impact your borrowing power, interest rates, and overall financial opportunities. Despite its significance, many individuals do not fully understand how credit scores work, how they are calculated, or how they affect various aspects of financial life.

If you are in any of these categories, you are just in the right place! In this comprehensive guide, we will break down the fundamentals of credit scores, discuss the different scoring models, explore the factors that influence credit scores, and provide insights on how to maintain a strong credit profile. Ready to learn every bit of it? Continue reading.

What Is a Credit Score?

A credit score is a three-digit number that represents your creditworthiness. It is based on your credit history and helps lenders determine the level of risk associated with lending you money. A high credit score signals responsible credit management, making it easier to qualify for loans, credit cards, and favorable interest rates.

Credit scores typically range from 300 to 850. The higher your score, the better your financial opportunities. A low score can result in loan denials, higher interest rates, and stricter borrowing conditions.

How Are Credit Scores Calculated?

Credit scores are calculated based on information found in your credit report. The major credit bureaus—Experian, Equifax, and TransUnion—compile these reports, and scoring models use this data to generate your score. The most widely used scoring models are FICO and VantageScore.

Breakdown of FICO Score Calculation

Your FICO score is the most widely used credit score by lenders and is determined by five key factors. Understanding how these components impact your score can help you make informed financial decisions.

1. Payment History (35%) – Your Track Record of On-Time Payments

Your payment history is the most significant factor in your credit score calculation. Lenders want to see a consistent pattern of on-time payments, as it indicates reliability in repaying debts. Here’s how different payment behaviors affect your score:

- On-Time Payments – A long history of making payments on time strengthens your credit profile. Even a single late payment can cause a significant drop in your score.

- Late or Missed Payments – Payments that are 30, 60, or 90 days late negatively impact your score, with longer delays causing greater damage.

- Collections & Charge-Offs – Accounts sent to collections or debts that are written off by lenders due to non-payment can significantly hurt your credit score.

- Bankruptcies & Foreclosures – These are considered severe derogatory marks and can stay on your credit report for up to 10 years.

To maintain a strong score, always pay at least the minimum amount due on time, and set up automatic payments or reminders to avoid missing due dates.

2. Amounts Owed (30%) – Managing Your Credit Utilization

The second most critical factor is the amount of credit you owe in relation to your total available credit, also known as credit utilization. Lenders assess this to determine how dependent you are on borrowed money.

- Credit Utilization Ratio – This is calculated by dividing your total credit card balances by your total credit limits. Keeping this ratio below 30% is recommended, but for optimal scoring, staying under 10% is even better.

- High Balances & Maxed-Out Cards – Carrying large balances or maxing out your credit cards signals financial risk and can cause a significant drop in your score.

- Debt-to-Income Ratio (DTI) – Although not part of your credit score calculation, lenders consider your total debt compared to your income when evaluating loan applications.

Pro-Tip: Pay down balances before your credit card statement closing date to lower your reported utilization and boost your score.

3. Length of Credit History (15%) – The Benefit of Longevity

A longer credit history demonstrates a track record of responsible credit use. This factor considers:

- Age of Your Oldest Account – A longer credit history provides more data on your financial habits, so keeping old accounts open (even if not frequently used) helps maintain a strong score.

- Average Age of All Accounts – Opening multiple new accounts in a short period lowers your average account age, which can negatively impact your score.

- Consistency Over Time – Maintaining open and active accounts responsibly over several years builds trust with lenders.

Pro-Tip: If you have an older credit card with no annual fee, keep it open to maintain a longer credit history.

4. Credit Mix (10%) – Diversity in Your Credit Portfolio

Lenders like to see a variety of credit types because it demonstrates your ability to manage different forms of debt responsibly. A well-balanced mix may include:

- Revolving Credit – Credit cards and lines of credit with variable monthly payments.

- Installment Loans – Fixed-term loans such as auto loans, mortgages, student loans, and personal loans.

- Retail Accounts – Store credit cards and financing options.

- Other Accounts – Credit-builder loans, secured credit cards, or finance company accounts.

Having a mix of both revolving and installment credit can positively impact your score, but opening new accounts just to diversify your mix is not recommended unless necessary.

5. New Credit Inquiries (10%) – The Impact of Credit Applications

Each time you apply for new credit, lenders conduct a hard inquiry (or "hard pull") on your credit report, which may slightly lower your score.

- Multiple Hard Inquiries – If you apply for several credit cards or loans in a short period, lenders may view you as a higher risk, causing a temporary dip in your score.

- Rate Shopping Protection – When applying for auto loans, mortgages, or student loans, multiple inquiries within a short window (typically 14-45 days) are often counted as a single inquiry to avoid penalizing consumers for rate shopping.

- Soft Inquiries – Checking your own credit report or receiving pre-approved offers does not affect your score.

Pro-Tip: Space out new credit applications and only apply when necessary to avoid unnecessary score reductions.

VantageScore Model Differences

While FICO remains the most commonly used scoring model, VantageScore is another widely recognized credit scoring system. Although both models evaluate similar factors, there are key differences:

1. Different Weighting of Factors

Unlike FICO, which gives the most weight to payment history and amounts owed, VantageScore places greater emphasis on:

- Total credit usage, balances, and available credit – VantageScore considers how well you manage your available credit over time.

- Credit behavior and trends – Instead of focusing on isolated factors, VantageScore evaluates how your credit activity changes over time.

2. Shorter Credit History Consideration

VantageScore can generate a score for consumers with a limited credit history (as short as one month), while FICO typically requires at least six months of credit history.

3. More Forgiving Approach to Hard Inquiries

VantageScore treats multiple inquiries differently. Instead of requiring inquiries to be grouped within a specific window, VantageScore considers all hard inquiries within a 14-day period as a single inquiry, regardless of the credit type.

4. Scoring Ranges and Versions

Both models use a range of 300-850, but individual scoring criteria differ slightly between different versions of FICO and VantageScore. Some lenders use older models, while others adopt newer versions with refined scoring algorithms.

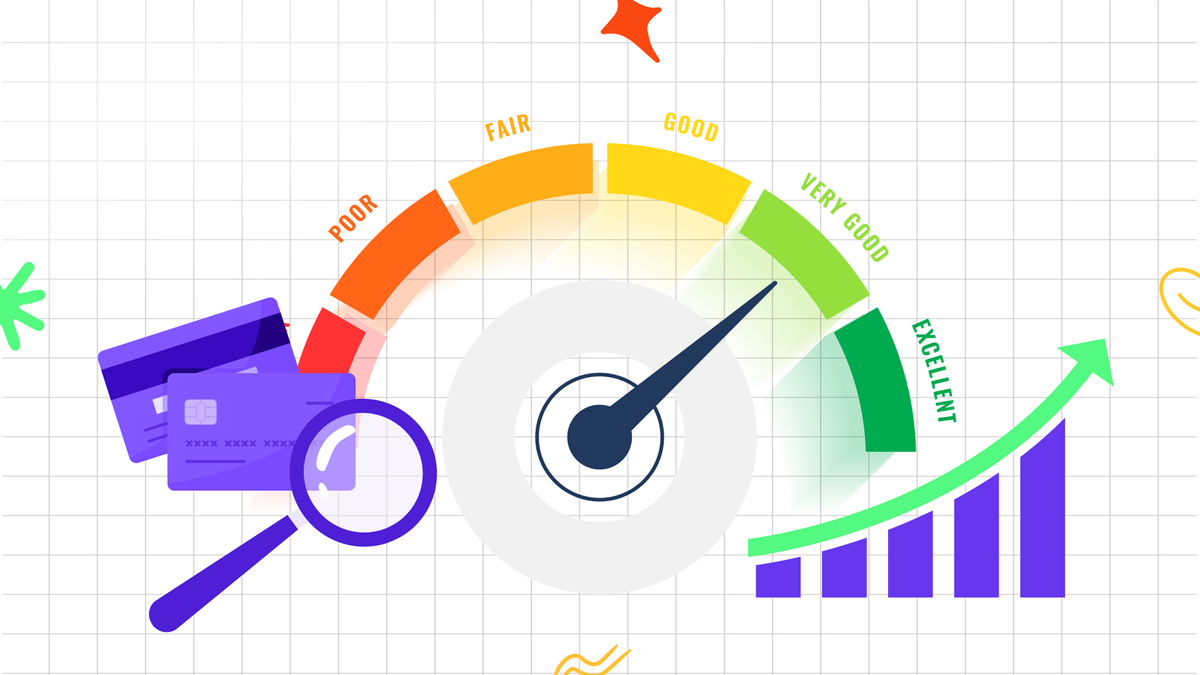

The Different Credit Score Ranges

Credit scores fall within the following ranges:

- 300-579 (Poor) – High risk to lenders; likely to be denied credit or given high-interest rates.

- 580-669 (Fair) – Considered subprime; may qualify for credit, but with unfavorable terms.

- 670-739 (Good) – Considered a reliable borrower; eligible for competitive interest rates.

- 740-799 (Very Good) – Lower risk; qualifies for better credit offers and terms.

- 800-850 (Excellent) – Exceptional creditworthiness; enjoys the best interest rates and terms.

Factors That Influence Your Credit Score

- Late Payments – Even a single late payment can have a significant negative impact.

- Credit Utilization Ratio – Keeping your credit card balances below 30% of your credit limit is recommended.

- Credit Inquiries – Too many hard inquiries can reduce your score.

- Closed Accounts – Closing old accounts can shorten your credit history and lower your score.

- Debt-to-Income Ratio – High debt compared to your income can affect your ability to take on new credit.

- Public Records – Bankruptcies, tax liens, and judgments negatively impact your score.

How Your Credit Score Affects You

- Loan Approvals & Interest Rates – Higher scores lead to better loan terms and lower interest rates.

- Credit Card Benefits – A strong credit score gives access to premium rewards and higher limits.

- Employment Opportunities – Some employers check credit reports for financial responsibility.

- Rental Applications – Landlords use credit scores to assess rental applications.

- Insurance Premiums – Some insurers adjust rates based on credit risk.

How to Improve Your Credit Score

- Make Payments on Time – Avoid late payments and set up autopay if necessary.

- Reduce Credit Utilization – Aim to keep balances below 30% of your total credit limit.

- Avoid Unnecessary Credit Inquiries – Only apply for new credit when absolutely necessary.

- Dispute Credit Report Errors – Regularly review your credit report for inaccuracies.

- Build a Positive Credit History – Keep old accounts open and manage them responsibly.

Conclusion

Understanding your credit score and how it impacts your financial life is essential for making informed financial decisions. By actively managing your credit and adopting responsible financial habits, you can maintain a strong credit score and enjoy better financial opportunities.

Looking to repair or improve your credit? Sign up for Credit Veto’s free credit repair starter guide today, take advantage of our flat-rate credit repair packages and take control of your financial future.

Comments ()