How Much Does Credit Score Decrease After a Car Loan? 2026 Top Tips 6 min read Credit Report Improve credit score How Much Does Credit Score Decrease After a Car Loan? 2026 Top Tips Credit Veto 2 days ago

How Long Do Late Payments Stay on Your Credit Report? 2026 Update 5 min read Improve credit score Credit Report How Long Do Late Payments Stay on Your Credit Report? 2026 Update Credit Veto 6 days ago

How Many Credit Cards Should I Have? Avoid These 4 Mistakes 12 min read Improve credit score How Many Credit Cards Should I Have? Avoid These 4 Mistakes Credit Veto 1 week ago

How to Check Personal Credit Report: 7 Easy Steps 9 min read Credit Report How to Check Personal Credit Report: 7 Easy Steps Credit Veto 1 week ago

How a Credit Repair Course Can Improve Your Credit Score and Business Faster 6 min read Credit repair Credit repair business Improve credit score How a Credit Repair Course Can Improve Your Credit Score and Business Faster Credit Veto 2 weeks ago

How Fast Will a Car Loan Raise My Credit Score? 2026 Real Timeline 7 min read Credit repair Credit Report Improve credit score How Fast Will a Car Loan Raise My Credit Score? 2026 Real Timeline Credit Veto 2 weeks ago

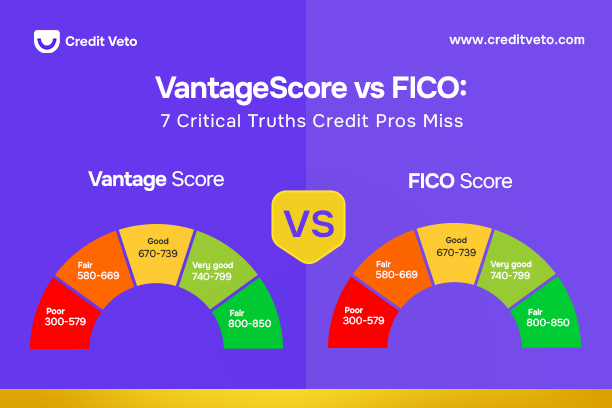

Vantage Score vs FICO: 7 Critical Truths Credit Pros Miss 10 min read Improve credit score Credit repair business Vantage Score vs FICO: 7 Critical Truths Credit Pros Miss Credit Veto 2 weeks ago

How to Read a Business Credit Report: 5 Key Tips for Success 6 min read Credit Report How to Read a Business Credit Report: 5 Key Tips for Success Credit Veto 3 weeks ago

How to Read a TransUnion Credit Report (Your Complete Guide) 7 min read Credit Report How to Read a TransUnion Credit Report (Your Complete Guide) Credit Veto 3 weeks ago

What Credit Score Is Needed to Buy a UTV? (Real Limits) 7 min read Credit repair Improve credit score What Credit Score Is Needed to Buy a UTV? (Real Limits) Credit Veto 3 weeks ago

How Long Do Late Payments Stay on Your Credit Report? 2026 Update

How Long Do Late Payments Stay on Your Credit Report? 2026 Update  How Many Credit Cards Should I Have? Avoid These 4 Mistakes

How Many Credit Cards Should I Have? Avoid These 4 Mistakes  How to Check Personal Credit Report: 7 Easy Steps

How to Check Personal Credit Report: 7 Easy Steps  How a Credit Repair Course Can Improve Your Credit Score and Business Faster

How a Credit Repair Course Can Improve Your Credit Score and Business Faster  How Fast Will a Car Loan Raise My Credit Score? 2026 Real Timeline

How Fast Will a Car Loan Raise My Credit Score? 2026 Real Timeline  Vantage Score vs FICO: 7 Critical Truths Credit Pros Miss

Vantage Score vs FICO: 7 Critical Truths Credit Pros Miss  How to Read a Business Credit Report: 5 Key Tips for Success

How to Read a Business Credit Report: 5 Key Tips for Success  How to Read a TransUnion Credit Report (Your Complete Guide)

How to Read a TransUnion Credit Report (Your Complete Guide)  What Credit Score Is Needed to Buy a UTV? (Real Limits)

What Credit Score Is Needed to Buy a UTV? (Real Limits)  How Long Do Late Payments Stay on Your Credit Report? 2026 Update

How Long Do Late Payments Stay on Your Credit Report? 2026 Update  How Many Credit Cards Should I Have? Avoid These 4 Mistakes

How Many Credit Cards Should I Have? Avoid These 4 Mistakes  How to Check Personal Credit Report: 7 Easy Steps

How to Check Personal Credit Report: 7 Easy Steps