Credit Report Dispute Letter: Powerful Template That Gets Results Fast

If you are trying to fix your credit, learning how to write a credit report dispute letter is one of the most important steps you can take. Many people have errors on their credit report, but the problem is not just the error itself. The problem is that most people do not know how to challenge it the right way.

A credit report dispute letter helps you clearly explain what is wrong on your report, provide proof, and request that the error be removed or corrected. When done properly, it can help fix incorrect accounts, remove outdated information, and improve your overall credit profile.

The issue is that many dispute letters get ignored or rejected. This usually happens because they are too vague, missing key details, or written using generic templates that do not match the situation.

In this article, you will learn exactly how to write a credit report dispute letter that works. You will also get a simple template you can use, understand what to include, and see how to improve your chances of getting results.

Read Also: How to Check Personal Credit Report: 7 Easy Steps

What Is a Credit Report Dispute Letter

A credit report dispute letter is a written request you send to a credit bureau or lender to correct information on your credit report that you believe is wrong. In the letter, you explain the error, provide supporting documents, and ask for the item to be removed or updated.

You should use a credit report dispute letter when you want to create a clear record of your request, especially if you have proof like payment receipts, bank statements, or identity documents. This method is often more effective than quick online disputes because it allows you to fully explain your case.

Once your dispute is received, the credit bureau usually has about 30 days to investigate. If the information cannot be verified, it must be corrected or removed from your credit report under federal law.

Key Steps to Using a Credit Report Dispute Letter

- Identify the error on your credit report

- Gather documents that prove the mistake

- Write a clear and specific dispute letter

- Send it to the correct credit bureau or company

- Wait for the investigation and review the result

What Makes a Dispute Letter Effective

An effective credit report dispute letter is:

- Clear and specific about the error

- Supported with real evidence

- Focused on one issue at a time

- Easy for the credit bureau to understand

When these elements are present, your chances of getting the error removed increase.

Why a Credit Report Dispute Letter Matters

Your credit report affects many parts of your life, from getting approved for loans to renting an apartment. If there is incorrect information on your report, it can lower your credit score and reduce your chances of getting approved.

A credit report dispute letter helps you challenge that information in a clear and structured way. When written properly, it shows exactly what is wrong and what action you want the credit bureau to take.

Who You Send the Letter To

You can send a credit report dispute letter to:

- The credit bureau that is reporting the error

- The company that provided the information, such as a bank or lender

Both parties are required to investigate your claim once they receive your letter.

When This Method Is Better Than Online Disputes

Online disputes are faster, but they can be limited. A credit report dispute letter is often better when:

- You have detailed proof that needs explanation

- Your previous online dispute was rejected

- You want to keep a clear paper trail

- The issue is complex and needs more detail

Because you can fully explain your case, this method can improve your chances of getting a correct outcome.

What Makes It Different from a Simple Complaint

A credit report dispute letter is not just a complaint. It is a structured request backed by evidence.

You are not just saying something is wrong. You are:

- Identifying the exact issue

- Explaining why it is incorrect

- Providing proof

- Asking for a specific correction

This is what makes it more effective than a casual message or quick submission.

Why Understanding This First Matters

Before you start writing, it is important to understand what a credit report dispute letter really is and how it works.

When you understand its purpose, you are more likely to write it correctly and avoid the mistakes that cause many disputes to fail.

When You Should Use a Credit Dispute Letter

Not every credit issue requires a dispute letter, but there are situations where using a credit report dispute letter is the better choice.

Knowing when to use it can save you time and increase your chances of getting results.

When You Have Strong Proof

If you have clear documents that show something is wrong, a credit report dispute letter is a strong option.

For example, if you have:

- Payment receipts

- Bank statements

- Account closure letters

You can explain the issue clearly and attach your proof. This makes your dispute stronger than a simple online submission.

When the Error Is Complex

Some credit report errors are not simple.

They may involve:

- Multiple accounts

- Identity theft

- Incorrect balances over time

In these cases, you need space to explain the situation properly. A credit report dispute letter allows you to give full details instead of selecting limited options in an online form.

When an Online Dispute Did Not Work

If you have already tried disputing online and nothing changed, sending a letter can be a better next step.

It shows that you are serious about the issue and gives you another chance to present your case more clearly with better documentation.

When You Want a Paper Trail

A credit report dispute letter creates a record.

When you send it, especially by certified mail, you have proof that:

- Your dispute was sent

- It was received

- It is being processed

This can be useful if there are delays or if you need to follow up later.

When You Are Dealing with Identity Theft

If someone has used your information without your permission, a dispute letter is often necessary.

You may need to include:

- Identity theft reports

- Police reports

- Proof of identity

A detailed letter helps explain the situation and supports your request for removal of fraudulent accounts.

When You Want More Control Over Your Dispute

Online forms guide you through fixed steps, but they can limit how much you explain.

With a credit report dispute letter, you are in control.

You decide how to present your case, what to include, and how to support your claim. This can make a big difference, especially if the issue is not straightforward.

Why Choosing the Right Method Matters

Using the right method at the right time can improve your results.

A credit report dispute letter is not always required, but when used correctly, it can be one of the most effective ways to dispute credit report errors and get them corrected.

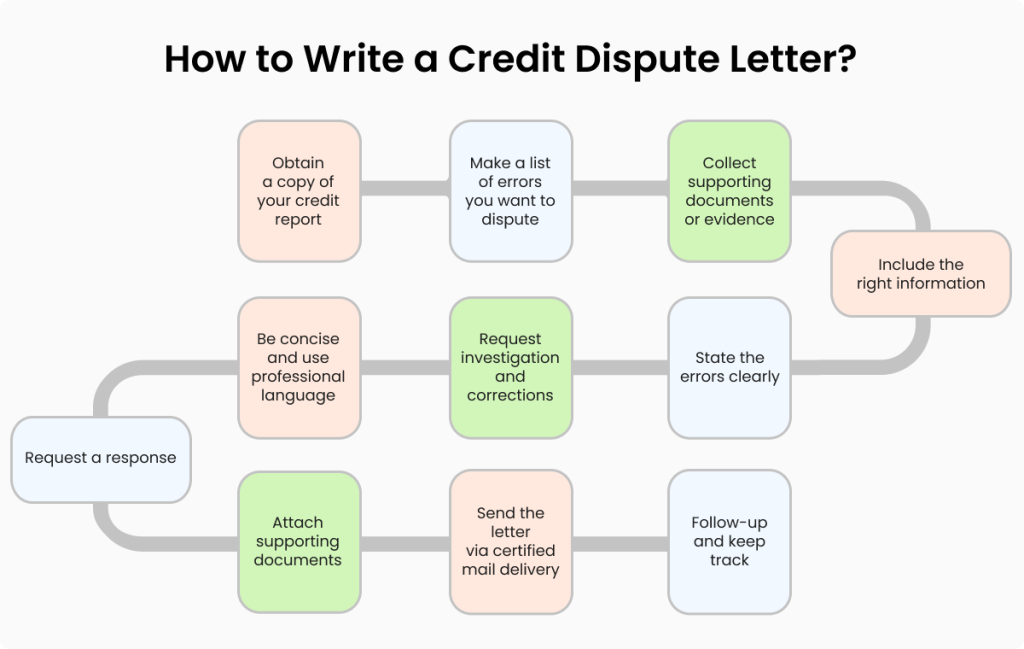

What to Include in a Credit Report Dispute Letter

Before you write a credit report dispute letter, you need to know what to include. Missing important details is one of the main reasons disputes get ignored or rejected.

A strong letter is simple, clear, and complete. It gives the credit bureau everything they need to understand the problem and take action.

Your Personal Information

Start your letter with your basic details so the credit bureau can identify your file.

Include:

- Your full name

- Your current address

- Your date of birth

- The last four digits of your Social Security number

Make sure this information matches what is on your credit report.

The Account or Item You Are Disputing

Next, clearly identify the exact item you want to dispute.

Include details like:

- Account name

- Account number

- The section of the credit report where it appears

Being specific helps avoid confusion and speeds up the investigation.

A Clear Explanation of the Error

This is one of the most important parts of your letter.

Explain:

- What is wrong

- Why it is incorrect

- What the correct information should be

Keep your explanation simple and direct. Avoid long or emotional statements. Focus only on facts.

Supporting Documents

Your dispute is stronger when you include proof.

Attach copies of documents such as:

- Payment receipts

- Bank statements

- Account letters

- Identity documents if needed

Do not send original documents. Always send copies.

What You Want Them to Do

Be clear about the action you expect.

For example, you can request:

- Removal of the item

- Correction of the information

- Update of account details

This helps the credit bureau understand exactly what you are asking for.

A Copy of Your Credit Report

Include a copy of your credit report with the error highlighted.

This makes it easier for the reviewer to locate the issue quickly and process your request faster.

Your Signature and Date

End your letter with your signature and the date.

This confirms that the request is coming from you and makes your dispute more official.

Why Each Part Matters

Every part of a credit report dispute letter has a purpose.

When your letter includes all the right details, it becomes easier for the credit bureau to investigate and respond. When something is missing, it can slow down the process or lead to rejection.

Keep It Simple and Focused

You do not need to write a long letter.

A good credit report dispute letter is:

- Clear

- Specific

- Supported with proof

The goal is to make your case easy to understand and easy to act on.

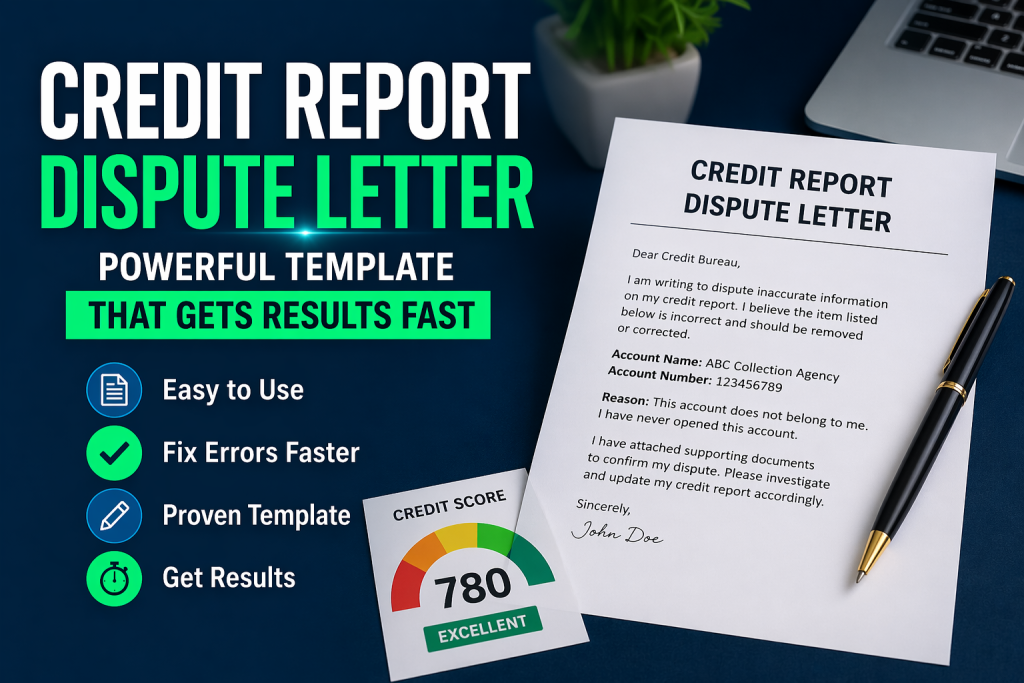

Credit Report Dispute Letter Template

Below is a simple credit report dispute letter template you can copy and use. You can adjust it based on your situation and the type of error you are disputing.

Sample Credit Report Dispute Letter

[Your Full Name]

[Your Address]

[City, State, ZIP Code]

[Date of Birth]

[Last 4 digits of SSN]

[Date]

[Credit Bureau Name]

[Credit Bureau Address]

Subject: Credit Report Dispute

Dear Sir or Madam,

I am writing to dispute the following information on my credit report. I believe this item is inaccurate and should be corrected or removed.

The details of the account are as follows:

Account Name: [Name of creditor]

Account Number: [Account number]

The issue is that this information is incorrect. [Explain clearly what is wrong. For example, this account does not belong to me, or this payment was made on time but reported late.]

I have attached copies of documents to support my claim. These documents show that the information reported is not accurate.

I am requesting that this item be reviewed and removed or corrected as soon as possible.

Please investigate this matter and provide me with an updated copy of my credit report once the changes have been made.

Thank you for your time and attention to this matter.

Sincerely,

[Your Signature]

[Your Full Name]

How to Use This Template

You should not copy this template word for word without making changes.

Instead, you should:

- Replace all placeholder sections with your real information

- Adjust the explanation to match your exact situation

- Attach the correct supporting documents

The more your letter matches your specific case, the stronger your dispute will be.

When This Template Works Best

This credit report dispute letter template works well when:

- You are disputing one clear error

- You have supporting documents

- You want to send your dispute by mail

If your case is more complex, you may need to expand the explanation slightly, but keep it clear and focused.

Why This Template Is Effective

This template works because it is:

- Simple and easy to read

- Direct and focused on the issue

- Supported with evidence

- Clear about the action you want

Credit bureaus handle many disputes every day. When your letter is easy to understand, it is more likely to be processed correctly.

A Smarter Way to Create Dispute Letters

Writing a credit report dispute letter manually can still be challenging, especially if you are unsure how to phrase your explanation or what details to include.

This is where tools like Credit Veto can help. Instead of starting from scratch, it generates personalized dispute letters based on your credit report, making the process easier and more structured.

How to Write a Credit Dispute Letter That Gets Results

Having a template is helpful, but what really makes a difference is how you use it. Many people send out dispute letters and get no results, not because they are wrong, but because their letter is not strong enough.

If you want your credit report dispute letter to work, you need to focus on clarity, accuracy, and proof.

Be Clear and Direct

Do not try to write too much or sound complicated.

Say exactly what the problem is and why it is wrong. For example, if an account does not belong to you, state it clearly. If a payment was reported late by mistake, explain the correct date and include proof.

The easier your letter is to understand, the easier it is for the credit bureau to act on it.

Focus on One Issue at a Time

It may be tempting to include multiple problems in one letter, but this can reduce clarity.

It is better to focus on one clear issue per letter. This makes your request easier to review and increases your chances of getting a correct result.

Use Real Evidence

A strong dispute is backed by proof.

Always attach documents that support your claim. This could be payment records, account statements, or official letters. Without evidence, your dispute may be verified and left unchanged.

Think of your letter as a case you are presenting. The stronger your evidence, the better your chances.

Keep Your Tone Professional

Your letter should be calm and respectful.

Avoid emotional language or long complaints. Focus on facts and what needs to be corrected. A professional tone makes your request easier to process and shows that you understand the process.

Avoid Generic Copy and Paste Letters

Many people use templates they find online without making changes.

This can weaken your dispute. Credit bureaus see many similar letters every day, and generic wording can make your request look less serious.

Always adjust your letter to match your exact situation.

Be Specific About What You Want

Do not just point out the error. State clearly what you want to happen.

For example, you can request that the item be removed, corrected, or updated. This helps the credit bureau understand your request and take the right action.

Follow Up If Needed

Sending your letter is not the final step.

After the investigation period, check your credit report to see if the issue has been resolved. If not, you may need to send another letter with stronger proof or more details.

Consistency is often what leads to results.

Why Most Dispute Letters Fail

Most credit report dispute letters fail because they are:

- Too vague

- Missing proof

- Not specific enough

- Not followed up properly

When you avoid these mistakes and follow the right approach, your chances of success improve.

A Better Way to Get It Right

Writing a strong credit report dispute letter takes time and attention to detail.

If you are unsure how to structure your letter or want to avoid mistakes, using a system like Credit Veto can help. It creates personalized letters based on your credit report, making sure the details are clear, accurate, and properly structured.

Where to Send Your Dispute Letter

Writing a strong credit report dispute letter is only part of the process. Sending it to the right place is just as important. If your letter goes to the wrong party, it may be ignored or delayed.

To get results, you need to know exactly who to contact.

Send It to the Credit Bureaus

You should send your credit report dispute letter to the credit bureau that is reporting the error.

The three major credit bureaus are:

- Experian

- Equifax

- TransUnion

Check your credit report to see which bureau is showing the incorrect information. If the same error appears on multiple reports, you should send a dispute letter to each bureau.

Send It to the Company That Reported the Information

In addition to the credit bureau, you can also send your dispute letter directly to the company that provided the information.

This could be:

- A bank

- A credit card company

- A loan provider

- A collection agency

These companies are known as “data furnishers,” and they are also required to investigate your dispute.

Why Sending to Both Can Help

Sending your credit report dispute letter to both the credit bureau and the reporting company can improve your chances of getting results.

This is because:

- The credit bureau investigates the report

- The company verifies the data

If both review your claim, the issue may be resolved faster and more accurately.

Use Certified Mail for Better Tracking

When sending your dispute letter by mail, it is best to use certified mail with a return receipt.

This gives you proof that:

- Your letter was sent

- It was received

- The date it was delivered

This record can be useful if you need to follow up or escalate the issue later.

Keep Copies of Everything

Always keep copies of:

- Your dispute letter

- Your supporting documents

- Your delivery confirmation

Staying organized helps you track your progress and respond quickly if needed.

Why This Step Matters

Even a well-written credit report dispute letter can fail if it is not sent correctly.

When you send your letter to the right parties and keep proper records, you make it easier for your dispute to be reviewed and resolved.

Common Mistakes That Get Dispute Letters Ignored

Writing a credit report dispute letter is not enough on its own. Many people send letters and expect results, but nothing changes. This is not because the system does not work. It is often because of small mistakes that weaken the dispute.

If you want your credit report dispute letter to be taken seriously, you need to avoid these common issues.

Writing Without Proof

One of the biggest mistakes is sending a dispute letter without any supporting documents.

A credit bureau will not remove an item just because you say it is wrong. They need proof. If your letter does not include documents like payment records or account statements, your dispute may be verified and left unchanged.

A strong dispute is always backed by evidence.

Being Too Vague

Some people write letters that are not clear.

For example, saying “this account is wrong” is not enough. You need to explain what is wrong, why it is wrong, and what should be done instead.

When your explanation is vague, it becomes harder for the credit bureau to understand your request and act on it.

Using Generic Templates Without Editing

Templates can help, but using them without making changes is a mistake.

Credit bureaus see many similar letters every day. When your letter looks generic and does not match your situation, it may not be taken seriously.

Your dispute should reflect your specific case, not a copied format.

Disputing Accurate Information

Not all negative information can be removed.

If the information is correct, it will remain on your credit report. Disputing accurate items can waste time and reduce the effectiveness of your future disputes.

It is better to focus only on real errors that can be proven.

Sending Everything at Once

Trying to fix everything in one letter can make your dispute confusing.

When too many issues are included, it becomes harder to review each one properly. This can slow down the process or lead to incomplete results.

It is better to focus on one clear issue at a time.

Not Following Up

Many people send a dispute letter and then do nothing.

If the issue is not resolved, you may need to follow up with another letter or provide more proof. Without follow-up, some disputes remain unresolved.

Consistency is a key part of getting results.

Why Most People Struggle With This Process

At this point, many people realize that writing a credit report dispute letter is not as simple as it seems.

You need to:

- Identify the right errors

- Gather the right documents

- Write clearly and correctly

- Track your disputes

- Follow up when needed

Missing any of these steps can affect your results.

Where Most People Get Stuck

The biggest challenge is not starting the process.

It is doing everything correctly and staying consistent from beginning to end.

This is why many people either give up halfway or keep repeating the same mistakes without seeing progress.

A Smarter Way to Handle Dispute Letters

Instead of guessing what to write or worrying about making mistakes, many people choose a more structured approach.

This is where Credit Veto starts to make sense. It removes the guesswork by helping you generate personalized dispute letters based on your credit report, so you are not relying on generic templates or incomplete information.

Should You Use a Template or a System

By now, you have seen how a credit report dispute letter works and what it takes to get results. The next question is simple. Should you write the letter yourself using a template, or should you use a system to help you?

The answer depends on your situation, your time, and how confident you are with the process.

Using a Template on Your Own

A template is a good starting point.

It gives you a basic structure and helps you understand what a credit report dispute letter should look like. If your case is simple and you are comfortable writing and organizing your documents, this approach can work.

However, you still need to:

- Identify the correct errors

- Adjust the template to match your situation

- Attach the right documents

- Track your disputes and follow up

This means you are responsible for every step of the process.

The Challenges of Doing It Yourself

Even with a template, many people run into problems.

They may:

- Miss important details

- Write unclear explanations

- Use the wrong supporting documents

- Lose track of their disputes

These small issues can lead to delays or rejected disputes, even when the person is right.

The process itself is not difficult, but it requires consistency and attention to detail.

Using a System Instead

A system is designed to guide you through the process and reduce mistakes.

Instead of starting from scratch, it helps you:

- Identify possible errors on your credit report

- Generate a credit report dispute letter based on your situation

- Keep everything organized in one place

- Track your progress and next steps

This makes the process more structured and easier to manage.

Where Credit Veto Fits In

This is where Credit Veto becomes useful.

Instead of relying on a general template, it creates personalized dispute letters based on your credit report. This means your letter is tailored to your exact situation, not copied from a generic format.

It also helps you stay organized and track your disputes, which is one of the biggest challenges people face when doing it manually.

For many people, the value is not just in writing the letter. It is in making sure the entire process is handled correctly from start to finish.

Which Option Is Better for You

If you have a simple case and you are comfortable handling everything yourself, a template may be enough.

If you want a more structured approach and want to reduce mistakes, using a system can make the process easier and more consistent.

The goal is not just to send a credit report dispute letter. The goal is to get results.

See Also: Best Credit Repair Software for Credit Repair Business

Writing a credit report dispute letter is one of the most effective ways to fix errors on your credit report. When done correctly, it allows you to clearly explain the issue, provide proof, and request the exact correction you need.

The process itself is simple, but the results depend on how well you follow each step. Being clear, specific, and consistent can make a big difference in whether your dispute is accepted or ignored.

If you choose to handle it yourself, using a good template and the right documents can help you get started. If you prefer a more structured approach, using a system can make the process easier and reduce the chances of mistakes.

Credit Veto helps simplify this by generating personalized dispute letters and keeping everything organized, so you do not have to figure it out on your own.

If you are ready to fix errors on your credit report, start by reviewing your report today and taking action with a clear, well-written dispute letter.

FAQs

How long does a credit dispute take?

A credit dispute usually takes about 30 days to complete. After you submit your dispute, the credit bureau reviews your claim, contacts the company that reported the information, and investigates the issue. If they cannot verify the information, it must be corrected or removed. In some cases, it may take a little longer if more documents are needed or if the case is more complex.

What is the best credit dispute letter?

The best credit dispute letter is one that is clear, specific, and backed by proof. It should clearly identify the error, explain why it is incorrect, include supporting documents, and state exactly what action you want, such as removal or correction. A strong letter is simple, focused on one issue at a time, and tailored to your situation rather than copied from a generic template.

How do I know if my credit dispute was approved?

You will know your credit dispute was approved when the credit bureau sends you the results of the investigation showing that the item was removed or corrected. You can also confirm by checking your updated credit report. If the disputed item is no longer there or has been changed, your dispute was successful.

How to Remove Inaccurate Items from Your Credit Report Quickly

How to Remove Inaccurate Items from Your Credit Report Quickly  How to Dispute Credit Report Errors and Win in 2026

How to Dispute Credit Report Errors and Win in 2026  Why Did My Credit Score Drop After Paying Off Debt? Proven Fixes

Why Did My Credit Score Drop After Paying Off Debt? Proven Fixes  How to Fix a Low Credit Score Fast: What Works in 2026

How to Fix a Low Credit Score Fast: What Works in 2026  How to Remove Closed Accounts from Credit Report Fast

How to Remove Closed Accounts from Credit Report Fast  How to Dispute Credit Report Errors Online: A Complete Step-by-Step Guide

How to Dispute Credit Report Errors Online: A Complete Step-by-Step Guide  The Smartest AI Credit Repair Tool to Fix Your Credit Fast

The Smartest AI Credit Repair Tool to Fix Your Credit Fast  Best Credit Repair Companies That Are Worth Trusting

Best Credit Repair Companies That Are Worth Trusting